Caixin has noted that Chinese regulators demand tech giants end ‘instant retail’ subsidy war asChina intensifies a war on toxic competition as economy suffers. The“toxic competition” is across a range of key industries, from steel and coal to emerging sectors such as photovoltaics, lithium batteries, new-energy vehicles and eCommerce platforms.

While Chinese regulators might be able to succeed at curving some toxic competition practices among industry giants, I suspect they will face considerable cultural hurdles.

A recent episode of The China Show discussed what can best be described as a sort of “hive mind” that many people in China have e.g. one person opens up a hotpot or bubble tea shop, everyone sees it doing well, and decides to open one until the whole street is lined with them with everyone loosing money. The show’s hosts mentioned same happened in property with everyone starting to speculate in it leading to a massive property bubble…

Finally, I’m visiting USA (the almond harvest will be in a few weeks) – so posts might get published at different times (around yard/orchard/harvest etc work). Note that the Archive.Today website, one of the mostly commonly used sites for saving/viewing articles (denoted by 🗃️ emojis), is again acting up. A ⛔ by a 🗃️ denotes articles that may or may not become viewable or saveable in a few hours, etc…

$ = behind a paywall

🇨🇳 🇭🇰 China & Hong Kong Stock Picks (June 2025) Partially $

🇨🇳 China –Bosideng International Holdings, Xiaomi, ZhongAn Online P & C Insurance, Shanghai Henlius Biotech, Green Tea Group, Waterdrop, BaTeLab, Jiumaojiu International Holdings, RoboSense Technology, Sany Heavy Equipment International Holdings, BYD Company, Duality Biotherapeutics Inc, CGN Mining Co Ltd, NIO Inc., Aac Technologies Holdings, Black Sesame International Holding, CSPC Pharmaceutical Group & BYD Electronic International Co Ltd

🇭🇰 Hong Kong – Swire Properties Ltd, Luk Fook Holdings International Ltd, Hongkong Land Holdings Ltd, Budweiser Brewing Company APAC Ltd, Far East Consortium International Ltd, Tai Cheung Holdings Ltd, Vitasoy International Holdings Ltd, China Overseas Land & Investment Ltd, Cafe De Coral, HKR International Ltd, ESR Group, Hutchison Port Holdings Trust, DFI Retail Group Holdings Ltd, Link Real Estate Investment Trust & New World Development Co Ltd

CMB International Capital Corporation’s 20+ high conviction stock ideas –Geely Automobile, Xpeng Inc, Zoomlion Heavy Industry, Sany Heavy Equipment International Holdings,, Sany Heavy Industry, Atour Lifestyle Holdings, CGN Mining Co Ltd, JNBY Design, Luckin Coffee, Proya Cosmetics, China Resources Beverage Holdings (CR Beverage), BeiGene, Innovent Biologics, AIA Group Ltd, PICC Property and Casualty Co Ltd, Tencent, Alibaba, Trip.com, Greentown Service Group, Xiaomi, Aac Technologies Holdings, BYD Electronic International, Horizon Robotics, Will Semiconductor Co Ltd, BaTeLab, Naura Technology & Salesforce

🌐 EM Fund Stock Picks & Country Commentaries (July 27, 2025) Partially $

AI reality check, Made In China 2025 review, investing beyond Taiwan tech, Korean trip report, Vietnam/India updates, are PGMs set to surge, global debt review, June/Q2 fund updates, etc.

$ = Behind a paywall / 🗃️ = Link to an archived article / ⛔ = Article archiving may not be archivable anymore

🌏 Musings to multi-baggers and mercifully few lemons: A review of all our picks to date (Pyramids and Pagodas)

An unfiltered lookback on three years of emerging market investment write-ups – hits, misses and why each piece mattered

A mix of eclectic trades, long-shot bets, and the occasional multi-bagger (with mercifully few lemons) has made the journey worthwhile.

Source: Pyramids and Pagodas

🇯🇵 Asian Dividend Gems: Taiyo Kagaku (Asian Dividend Stocks) $

Although Taiyo Kagaku (NSE: 2902) is not a household name among consumers in Japan, it has a strong reputation in Japan and internationally among F&B companies for functional, health-enhancing ingredients.

Three main reasons we like the stock include strong loyal customers in the F&B segment in Japan/internationally, solid growth of sales and profits, and attractive valuations.

Taiyo Kagaku currently has a SmartScore of 4.6 out of 5 which is among the top ranking stocks in the Japanese stock market.

🇨🇳 How to Spot Red Flags in Chinese & HK Markets (The Great Wall Street)

AI Prompts to Avoid Value Traps and Streamline Stock Research

I’ll show you how AI-powered stock screening can transform your investment research, helping you quickly eliminate value traps in Chinese and HK markets by spotting hidden red flags like regulatory risks and balance sheet issues. In this guide, I’ll share proven AI prompts for stock analysis that save hours of manual work, focusing on business models, competitive moats, and forensic accounting to streamline your process and uncover genuine opportunities

🇨🇳 Chinese Investors Face 20% Tax Bill on Offshore Trading Profits (Caixin) $

China is stepping up enforcement of its long-standing tax rules on overseas investments, a move that indicates deeper scrutiny of the country’s expanding class of global retail investors.

Tax authorities across the country have begun proactively contacting individuals who trade U.S. and Hong Kong stocks, instructing them to declare their income and settle tax liabilities.

🇨🇳 In Depth: China Reopens the Door for Loss-Making Tech Startups to Go Public (Caixin) $

For two years, the door to China’s public markets remained firmly shut to companies that hadn’t yet turned a profit.

That changed in June, when Wu Qing, the chairman of the China Securities Regulatory Commission (CSRC), took the stage at the 2025 Lujiazui Forum with a market-shifting announcement: a new sci-tech growth tier would be added to the Nasdaq-style STAR Market, once again allowing pre-profit companies to list under the long-dormant fifth listing standard.

🇨🇳 Chinese Regulators Demand Tech Giants End ‘Instant Retail’ Subsidy War (Caixin) $

China’s market regulator has summoned three of the country’s top e-commerce platforms — Meituan (HKG: 3690 / 83690 / SGX: HMTD / FRA: 9MD / OTCMKTS: MPNGF / MPNGY), JD.com(NASDAQ: JD / SGX: HJDD) and Alibaba (NYSE: BABA)-backed Ele.me — in a bid to cool an escalating price war driven by aggressive subsidies.

The State Administration for Market Regulation (SAMR) issued a statement late Friday demanding the companies adhere to fair competition rules and engage in rational market behavior.

🇨🇳 In Depth: China Intensifies War on Toxic Competition as Economy Suffers (Caixin) $

Chinese policymakers are stepping up efforts to stamp out rampant “involution-style” competition across a range of key industries, from traditional areas such as steel and coal to emerging sectors such as photovoltaics, lithium batteries, new-energy vehicles (NEVs) and e-commerce platforms.

Since the Politburo, one of the country’s top decision-making bodies headed by President Xi Jinping, called out this destructive phenomenon at a meeting in July last year, addressing the problem has become a top priority because of the damage it’s causing to the economy by distorting market pricing, eroding corporate profit margins, and undermining industrial efficiency.

🇨🇳 Alibaba turns up its ‘instant retail’ game (Bamboo Works)

The merger of its Ele.me service with its core e-commerce business marks a new stage in the e-commerce giant’s three-way “on-demand retail wars” with Meituan (HKG: 3690 / 83690 / SGX: HMTD / FRA: 9MD / OTCMKTS: MPNGF / MPNGY)and JD.com(NASDAQ: JD / SGX: HJDD)

Alibaba (NYSE: BABA) has shut down its money-losing local services segment, absorbing its Ele.me takeout dining service into its main e-commerce business group

On-demand commerce has become the company’s new mantra in its restructured e-commerce business as it shelves a previous breakup plan

🇨🇳 Will Meituan’s Keeta come to Singapore, or Southeast Asia? (Momentum Works)

Meituan (HKG: 3690 / 83690 / SGX: HMTD / FRA: 9MD / OTCMKTS: MPNGF / MPNGY)’s Keeta is aggressively planning its entry to Brazil, while expanding to Kuwait, Qatar and UAE, after becoming #2 in Saudi Arabia.

Lately we’ve often been asked: “Will Keeta expand to Singapore — or Southeast Asia more broadly?”

Both Keeta entities in Singapore seem to be holding, not operating, companies.

Is Singapore a relevant and attractive market for Meituan? Well, the market is small. Momentum Works Food Delivery Platforms in Southeast Asia report estimates Singapore’s food delivery GMV in 2024 to be US$2.6 billion – or about 4 days of Meituan’s GMV in China. But then Indonesia, the largest market in Southeast Asia, was only about 2 times bigger at US$5.4 billion.

We suspect that any market that has volume and density (in terms of population and spending power) is probably under Meituan’s radar. There are some exceptions – for example, India, which has banned most Chinese internet companies, and Japan, where omnipresent convenience stores fulfill everything.

🇨🇳 China to Put Alipay, Tenpay Under Tighter Anti-Money Laundering Scrutiny (Caixin) $

China’s central bank is moving to bring the country’s two payment giants, Ant Group Co. Ltd.’s Alipay and Tencent (HKG: 0700 / LON: 0LEA / FRA: NNND / SGX: HTCD / OTCMKTS: TCEHY)’s Tenpay, under its direct anti-money laundering supervision, a significant escalation in Beijing’s campaign to manage financial risk at its most systemically important institutions.

The move is part of a proposed regulatory overhaul that would subject 27 major financial firms — including top banks, brokerages and insurers — to the direct oversight of the People’s Bank of China’s (PBOC) headquarters for compliance with rules against money laundering and terrorism financing.

🇨🇳 JD.com Splashes Cash on Robotics AI Startups (Caixin) $

Three robotics startups announced Monday they had completed funding rounds led by JD.com(NASDAQ: JD / SGX: HJDD), signaling the Chinese e-commerce giant is accelerating its push into the burgeoning, much-hyped field of embodied artificial intelligence (AI).

Embodied AI — which refers to intelligent systems with physical forms that interact with the real world, such as robots and self-driving cars — has recently become a battleground for tech firms. As JD.com is a relative latecomer, it’s making an aggressive effort to catch up with rivals like Meituan (HKG: 3690 / 83690 / SGX: HMTD / FRA: 9MD / OTCMKTS: MPNGF / MPNGY) and Lenovo Group (HKG: 0992 / FRA: LHL / LHL1 / OTCMKTS: LNVGY / LNVGF).

🇨🇳 China lays out its AI vision in foil to Donald Trump’s ‘America First’ plan (FT) $ 🗃️

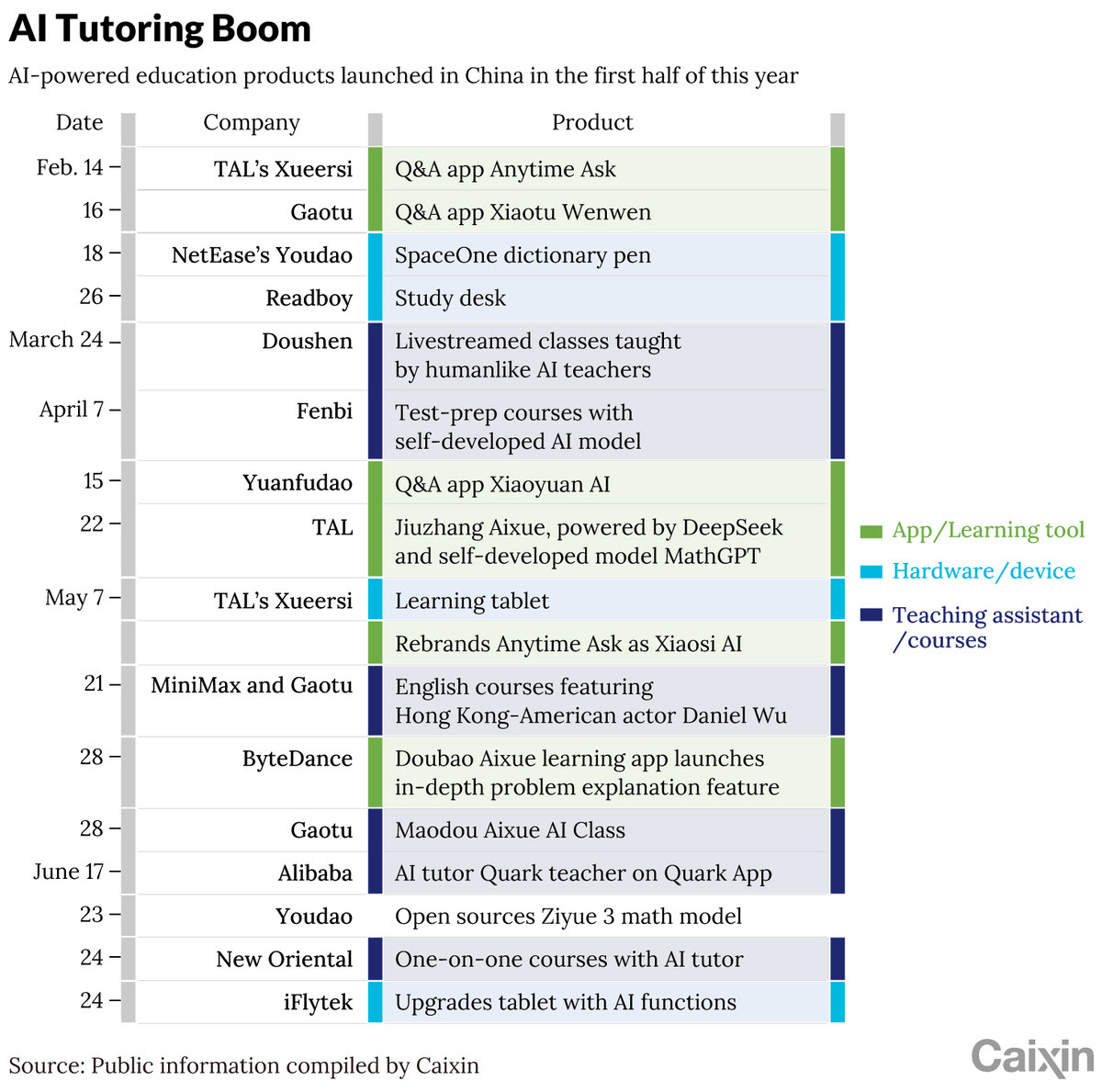

🇨🇳 In Depth: AI Foray Is Teaching China’s Edtech Firms a Valuable Lesson (Caixin) $

In recent years, tutoring apps powered by artificial intelligence (AI) have generated significant buzz by providing features such as English language training, math problem explanations and help with writing essays.

Many private education companies have scrambled to integrate large models developed by big names like ByteDance Ltd. and up-and-comers like DeepSeek into their AI-powered teaching apps to improve the user experience.

🇨🇳 Pony AI pulls ahead of WeRide in China robotaxi race (Bamboo Works)

Both companies notched an important new advance last week when Shanghai unveiled a major expansion to its robotaxi program

Pony AI Inc (NASDAQ: PONY), WeRide Inc (NASDAQ: WRD) and Baidu(NASDAQ: BIDU) were among groups awarded licenses to operate in a major expansion of Shanghai’s robotaxi program

Pony AI’s stock is up 16% since its U.S. listing last November, while WeRide has lost a third of its value since its Nasdaq trading debut a month earlier

🇨🇳 Falsifying Data Can’t Save You From Severe Competition: Why We Believe Pony AI Inc. is the Worst of the Robotaxi Hype (Grizzly Research LLC)

Pony AI Inc (NASDAQ: PONY) is a hyped robotaxi company that went public in November 2024. Recent rumors around interest by former Uber CEO Travis Kalanick in PONY’s U.S. business have driven excitement around the company.

Our research, including on-the-ground testing in one of the major cities in China and expert interviews, indicates that PONY has, in fact, very little to offer and is more akin to a smoke and mirrors show.

There are serious allegations from an apparent insider that PONY actively falsified data for the algorithm of its self-driving software. Management is allegedly aware of the issue and was covering it up. We find this reckless and dangerous, especially for a company that develops autonomous driving software.

While PONY likes to portray itself as an international player, the reality is that the company’s permit to conduct autonomous vehicle testing without a driver in California was revoked a few years ago after a crash. Pony had a similar incident in May 2025 in China, which reportedly led to the temporary suspension of the service in that district. It appears that PONY currently only has a permit to conduct autonomous vehicle testing with a driver in the U.S.

🇨🇳 Qidian Guofeng tries on ‘AI halo’ in move to boost business (Bamboo Works)

The company, which is developing an online-merge-offline (OMO) new consumption platform, swung to a 2.23 billion yuan loss last year on asset impairments

China Qidian Guofeng Holdings Ltd (HKG: 1280) has signed a letter of intent to acquire an AI technology company, sparking a rally for its shares

The company, which mostly engages in appliance and liquor trading, is making the move even as most AI operators continue to lose money

🇨🇳 Cover Story: A New Gold Rush Begins in China’s Hard Tech Sector (Caixin) $

On a quiet Sunday in mid-July, before the new week’s trading bells could ring, China’s financial regulators pulled off a quiet revolution.

The Shanghai Stock Exchange unveiled five regulatory notices and a Q&A on its website, officially launching a sci-tech growth tier — a new section within its tech-heavy Nasdaq-style STAR Market. Thirty-two loss-making tech firms were welcomed as its inaugural cohort. More are expected to follow.

🇨🇳 Lufax deepens Ping An reliance, as it works towards trading resumption (Bamboo Works)

The online loan facilitator has signed a flurry of agreements strengthening its ties to its parent, Ping An Group [Ping An Insurance (SHA: 601318 / HKG: 2318 / SGX: HPAD / OTCMKTS: PNGAY)], as it works towards reinstatement of trading for its Hong Kong stock

Lufax Holdings (NYSE: LU) has hired Ernst & Young as its new auditor after firing PwC over disagreements about related-party transactions

At the same time, the online loan facilitator disclosed a series of new agreements involving its parent, Ping An, to support its business growth

🇨🇳 Lithium price slump: the ghost that keeps haunting Ganfeng Lithium (Bamboo Works)

The producer of the key component used to make EV batteries expects to report a worse-than-expected loss in the first half of 2025, with no end in sight as prices remain low

Ganfeng Lithium Group (SHE: 002460 / HKG: 1772 / OTCMKTS: GNENY / GNENF)’s net loss, excluding non-recurring items, widened in the first half of 2025 from a year earlier

The producer of the key component used to make EV batteries and energy storage equipment is suffering as lithium prices continue to hover near cost levels

🇨🇳 Hengrui Pharma targets obesity drug launch after test success (Bamboo Works)

The Chinese drug company is looking to break into the big league for weight-loss treatments after its injection demonstrated sustained weight loss in Phase Three trials

Participants receiving the highest dose in the 48-week Chinese trial were said to lose up to 19.2% of their weight

The Jiangsu Hengrui Pharmaceuticals Co (SHA: 600276) drug targets the same receptors as Eli Lilly’s blockbuster product tirzepatide

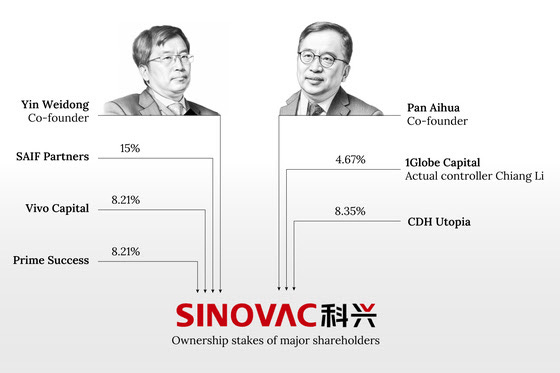

The Covid-19 pandemic turned Chinese vaccine-maker Sinovac Biotech Ltd (NASDAQ: SVA) into a global household name after its CoronaVac jab became a billion-dollar money-spinner and one of the world’s most-administered inoculations against the virus. But hidden away behind its success lies a bitter, decade-long power struggle for control of the company.

The founders of the Nasdaq-listed company and their institutional backers have been at war since a failed attempt to take the company private in 2016. The latest twist in the long-running drama came on July 8, when a special shareholder meeting (SM) requisitioned by a group of dissident shareholders to install a new board descended into chaos.

The company boosted sales of pre-owned products last year, leading to a 26% increase in its annual revenue

ATRenew (NYSE: RERE) handled sales of more than 35.3 million pre-owned smartphones and other products last year, up from 32.3 million in 2023

The company also set ambitious emissions reduction goals, aiming to cut Scope 1 and 2 emissions by 35% and Scope 3 emission by 50% by 2030 from 2024 levels

🇨🇳 Issue #7 : Undervalued Sportwear Company (Bargain Stocks Radar)

For this issue I thought I would share you with my research notes on a Hong Kong listed smid cap called 361 Degrees International Limited (HKG: 1361 / FRA: 36L / OTCMKTS: TSIOF).

The share price has increased by around 20% since I started researching. Despite this increase the shares still look undervalued.

361 Degrees is a Xiamen (China) based sportswear firm established in 2003 and listed on the Hong Kong Stock Exchange in 2009. The current market cap at time of publishing is 11.31 billion Hong Kong dollars ($1.44 billion USD).

The company designs, manufactures and distributes their own branded athletic footwear, apparel and accessories.

Overall 361 seems like a well-managed business that’s trading at a significant discount to peers and pays a nice dividend. The international expansion opens up the opportunity for continued growth in revenue and profits. With more liquidity being directed into Hong Kong stocks I feel 361 Degrees is flying ‘under-the-radar’ and could be worthy of further attention.

🇨🇳 Stella International steps sideways on flattening revenue, U.S. tariff threats (Bamboo Works)

The contract footwear maker’s shares rallied after it announced lukewarm second-quarter sales, possibly on bullish forward-looking comments from its largest customer, Nike

Shares of contract footwear maker Stella International Holdings Ltd (HKG: 1836 / FRA: 31S / OTCMKTS: SLNLY / SLNLF) rose nearly 10% in the four trading days after it issued a lackluster second-quarter business update

The company’s average selling price has been tracking downwards as it shuts down its retail operation and shifts away from casual brands to focus on athletic footwear

🇨🇳 Big US toymakers seek to diversify away from China as tariffs bite (FT) $ 🗃️

🇨🇳 Its Hong Kong listing advancing, will investors drink up Bama Tea shares? (Bamboo Works)

After three failed listing attempts, the tea leaf seller has received a key regulatory green light for its planned IPO from China’s securities watchdog

Bama Teach has been approved by China’s securities regulator for a Hong Kong IPO, but must renew its application after its original prospectus recently expired

The tea leaf seller is expected to refile for the listing soon, and could ring the Hong Kong Stock Exchange’s opening “gong” with a trading debut later this year

🇭🇰 CK Hutchison: Focus On Results Preview And Port Disposal(Seeking Alpha) $⛔🗃️

Laopu Gold Co Ltd (HKG: 6181)’s stock has fallen nearly 30% since its July 8 peak and declined another 4% yesterday despite an upbeat 1H2025 profit update.

The company’s positive profit alert reported revenues and profits up more than 2.5x year-on-year, exceeding market expectations.

The ongoing share price weakness despite strong results likely reflects a combination of technical factors, such as lock-up related selling, and broader fundamental concerns.

🇭🇰 MegaRobo Technologies IPO Valuation Analysis: Headed For $1B+ Public Market Debut In Hong Kong (Smartkarma) $

MegaRobo Technologies files for Hong Kong IPO and seeks fresh funding to expand production capacity, accelerate R&D efforts and improve working capital.

The rapidly growing autonomous agent provider in robotics applications in China did not disclose the proposed size and price range for the share sale in filings.

MegaRobo Technologies is enjoying healthy ~40% growth. I estimate the company’s TAM is ~$4.7B in 2024 and is expected to grow to ~$19B by 2030 only in China.

🇲🇴 Macau GGR to grow 9pct y-o-y in 2H: Seaport Research (GGRAsia)

Macau casino gross gaming (GGR) could expand by 9 percent-plus year-on-year in the second half, forecasts Seaport Research Partners.

This was due to the fact that “growth has reaccelerated in the last few months,” said senior analyst Vitaly Umansky in a Monday note.

Second-half 2024 GGR was just under MOP113.03 billion (US$13.98 billion), according to data from Macau’s Gaming Inspection and Coordination Bureau.

“In Macau, we now forecast GGR growth of 7 percent” for full-year 2025, stated Mr Umansky in his Monday update. The city’s full-year 2024 GGR came in at just over MOP226.78 billion.

🇲🇴 Macau 5-star room rate averages US$180 in June, marking 12 months in a row of y-o-y decline: trade (GGRAsia)

The average nightly cost in June of a Macau five-star hotel was down by 8.1 percent year-on-year to MOP1,454.0 (US$179.8). It represented the twelfth consecutive month – measured from July 2024 – of year-on-year decline in the five-star average rate.

That is according to the latest monthly survey from the Macau Hotel Association, published by the Macao Government Tourism Office.

The association currently has 47 hotels as members, of which 26 are five-star properties. Most of those are within casino resort complexes in the city. The rest of the association’s hotel members are of the four- and three-star tier.

Last month, the average room rate across all tiers of the association’s hotels stood at MOP1,261.4, down 8.8 percent year-on-year.

An “economic slowdown” was cited as a key factor in the 14.9-percent decline in gaming sector suspicious transaction reports (STRs) filed in the first half of 2025.

That is according to the Financial Intelligence Office – a unit of Macau’s Unitary Police Service – in an emailed reply to GGRAsia’s enquiry.

The Macau gaming sector filed an aggregate of 1,856 STRs in the first six months of this year. That compared with 2,181 STRs the sector filed in the prior-year period.

“The decrease in the number of STRs in gaming sector was mainly due to the economic slowdown,” stated the Financial Intelligence Office.

🇲🇴 MGM Resorts International MGM (Jon’s Thoughts)

Share repurchase monster

So we’ll dive directly into MGM Resorts International (NYSE: MGM)’s share repurchases, and I’ll get straight to the point: MGM has repurchased about 50% of its outstanding shares in the past 5 years.

MGM has a lot going for it. At this price, I think it is a compelling opportunity even without any future share repurchases. But I hope reading this has helped you understand why I chose to focus so much of the writing on MGM’s repurchase activity. The market is valuing MGM as if its future is bleak — not to mention giving the company no credit for its past repurchases which have cut the share count in half. I support the company’s action to take advantage of the opportunity the market is providing. People can disagree with one another about any company’s valuation and prospects, but at the end of the day, big share reductions and their ramifications are just numbers and arithmetic. When calculating per share metrics, the denominator is not a matter of opinion.

🇲🇴 Las Vegas Sands says room for better Parisian Macao and Sands Macao performance as looks to improve EBITDA (GGRAsia)

The Las Vegas Sands (NYSE: LVS) says it sees a particular opportunity for it “to perform better” at its smaller Macau properties The Parisian Macao in the Cotai district, and Sands Macao. The latter is the group’s first venue built in the city, located in downtown Macau.

The comment – on a Wednesday call with investment analysts to discuss the second quarter earnings of the group – was from Grant Chum Kwan Lock, chief executive and president of Sands China (HKG: 1928 / FRA: 599A / OTCMKTS: SCHYY / OTCMKTS: SCHYF), Las Vegas Sands’ Macau unit. He was explaining how the firm was working to recover market share, after in May commentary the group admitted it had not been aggressive enough on player reinvestment.

🇲🇴 Las Vegas Sands 2Q profit up 22pct y-o-y helped by Marina Bay Sands while Sands China net income down (GGRAsia)

Casino operator Las Vegas Sands (NYSE: LVS)reported net income of US$519 million in the second quarter, up 22.4 percent year-on-year, according to a Wednesday filing in the United States.

The latest result was based on net revenues that rose 15.0 percent year-on-year, to nearly US$3.18 billion.

The group operates casinos in Macau via its Sands China (HKG: 1928 / FRA: 599A / OTCMKTS: SCHYY / OTCMKTS: SCHYF) unit, and the Marina Bay Sands property (pictured in a file photo) in Singapore via its Marina Bay Sands Pte Ltd unit.

Group-wide casino revenues were up 18.7 percent year-on-year, to just under US$2.42 billion.

🇹🇼 Taiwan Semiconductor Has A Lofty Valuation With Risks (Seeking Alpha) $⛔🗃️

🇹🇼 Taiwan Semiconductor: The Saga Continues (Seeking Alpha) $⛔🗃️

🇹🇼 TSMC: Valuation Lags Behind The Fundamental Rally (Seeking Alpha) $⛔🗃️

🇹🇼 TSMC: Hot AI Demand Meets Capacity Crunch And Margin Erosion – Time To Take Profits? (Seeking Alpha) $⛔🗃️

🇹🇼 TSMC: Time To Hedge With Options (Rating Downgrade) (Seeking Alpha) $⛔🗃️

🇹🇼 TSMC: A No Brainer Long-Term Investment (Seeking Alpha) $⛔🗃️

🇹🇼 TSMC’s Q4 Prudence Is Temporary – Wait For A Dip Before Adding (Seeking Alpha) $⛔🗃️

🇹🇼 TSMC: Even Bull Runs Need To Take A Healthy Breather (Downgrade) (Seeking Alpha) $⛔🗃️

🇹🇼 ChipMOS Technologies: Could Soon Show The Path Ahead (Seeking Alpha) $⛔🗃️

🇹🇼 FX volatility, new capital rules push Taiwan insurers to adjust (The Asset) 🗃️

Focus on strengthening hedging tools, extending duration, investing in local assets

Taiwan’s insurers are facing heightened foreign exchange ( FX ) risk and stricter capital rules under the Taiwan Insurance Capital Standard ( TW-ICS ), scheduled to be implemented in 2026. As a result, strategic adjustments, such as strengthening FX hedging, extending duration and tapping locally advantaged alternatives, are essential to helping insurers navigate volatility while enhancing capital efficiency.

🇹🇼 Taiwan Semiconductor Manufacturing Company (Part 1) (Global Outperformers)

Most investment write-ups begin with bullish arguments. Here, I’ll flip the script.

Let me walk you through five reasons not to invest in Taiwan Semiconductor Manufacturing Company (TSMC) (NYSE: TSM), the world’s largest semiconductor foundry. Or why you might even want to short its stock.

🇹🇼 TSMC Earnings Review: Q2 2025 (Modern Value Investing)

Taiwan Semiconductor Manufacturing Company (TSMC) (NYSE: TSM) reported Q2-25 results on 17 July 2025. Revenue climbed to TWD 933.8 bn (≈ US$30.1 bn) while diluted EPS reached TWD 15.36, up ~39 % and 60.7 % year-on-year respectively . Both topline and bottom-line exceeded consensus, beating by 1.6 % and 5.9 %, respectively .

Management guides Q3-25 revenue of US$31.8–33.0 bn, +8 % QoQ and +38 % YoY at the midpoint, with gross margin of 55.5–57.5 % . This implies revenue 5–7 % above Visible Alpha consensus, but a 200-bps margin compression as overseas-fab dilution and further NT$ strength persist. Full-year revenue growth outlook was raised to “around 30 % in U.S. dollars” — ~5 pts above the Street.

🇰🇷 Potential Change in Taxes on Capital Gains on Stocks & Securities Transactions: Impact on Korean Stocks (Douglas Research Insights) $

The capital gains tax on stock sale gains and securities transaction taxes could be raised in 2H 2025, which could negatively impact the Korean stock market, especially small caps.

Combination of higher securities transaction tax and capital gains on stock sales could result in local retail investors selling their shares in 4Q 2025, before these changes come into effect.

Although many small caps in Korea have performed well this year, the potential changes on these two important taxes could put some damper on the recent excellent share price performances.

🇰🇷 Two New Tax Tweaks Set to Shake Up Korea’s Local Stock Market: Trading Tax & CGT Threshold (Smartkarma) $

Trading tax gradually dropped from 0.25% in 2020 to 0.15% in 2025, boosting volatility and short-term trades; a hike to 0.25% could cool momentum but widen arbitrage and basis spreads.

If the major shareholder tax threshold drops to ₩1B, year-end retail dumps and Jan buybacks will return—but with less wild swings and more measured short-term fade and momentum trades.

If the tax revamp drops end-July, expect a September Assembly push. Usually effective next January, but like 2023’s cap gains hike, changes might apply immediately in 2025.

🇰🇷 Korean Policy Tailwinds: Preferred Shares Rerating Play (Smartkarma) $

Most expect prefs to be in policy crosshairs soon—watch for tighter rules on dividends, discounts, and liquidity, plus likely incentives for redemption or cancellation ahead of commons.

If Korea rolls out a pref stock overhaul, long-biased rerate plays could pop—focus on liquid, high-yield large-cap prefs trading at 35%+, yield north of 3%, and solid daily turnover.

Korea Investment Holdings (KRX: 071050 / 071055), Kumho Petrochemical (KRX: 011780 / 011785), CJ Cheiljedang Corporation (KRX: 097950 / 097955), CJ Corp (KRX: 001040) prefs already screen well; Doosan and Hanwha 3PB could join if dividend hikes materialize on back of strong sub earnings.

🇰🇷 LG Display: Results Beat Reinforces My Bullish View(Seeking Alpha) $⛔🗃️

🇰🇷 Special Situation: Trading at Net Cash, 35% FCF Yield (Elias’ Investing Journal)

Short Term Investment Idea

DoubleDown Interactive (NASDAQ: DDI) is a South Korean game developer listed on Nasdaq. The company was founded in 2008 and transitioned to a social casino and gaming focus in 2017, after a majority stake was acquired by Doubleu Games Co Ltd (KRX: 192080), another Korean gaming firm.

Many will argue this is a typical value trap, where there is no price worth buying if management refuses to return cash to shareholders.

I agree it is a shame to do anything with the cash other than massive dividends and buybacks at this level.

However, I don’t think they need to for this to work out.

🇰🇷 Potential Adds & Deletes in the MSCI Korea Index in August 2025 As Highlighted by Locals in Korea (Douglas Research Insights) $

🇰🇷 Korea Small Cap Gem #41: Korea Fuel Tech (FT) Corp (Douglas Research Insights) $

Korea Fuel-Tech Corp (KOSDAQ: 123410) is the 41st company in our Korea Small Cap Gem Series.

Korea Fuel Tech (FT) Corp is a Korean automotive components manufacturer specializing in emissions control systems, fuel system parts, and other auto plastic parts.

Three key investment highlights include key beneficiary of growing demand for carbon canisters used in hybrid vehicles, compelling valuations, and sharp increase in operating margins/ROE.

🇰🇷 Makus: A Textbook Case Study of How Improving Shareholder Value Leads to Surging Share Price (Douglas Research Insights) $

Makus Inc (KOSDAQ: 093520) is a textbook case study in Korea of how improving shareholder value leads to surging share price. Its example is simple and beautiful.

Makus announced that it will cancel a total of 6 million treasury shares (37% of outstanding shares) in the next three years until 2027 to increase shareholder value.

Applying a 15x P/E on EPS of 2,788 won (2027E) results in implied target price of 41,820 won per share, which would be a 67% further upside from current levels.

🇰🇷 Korea Surpasses France as Top Exporter of Cosmetics to the USA [CJ Olive Young – Key Beneficiary] (Douglas Research Insights) $

Korea surpassed France as the top exporter of cosmetics to the USA in 2024. Korea exported $1.7 billion worth of cosmetics to the USA in 2024, up 54.2% YoY.

CJ Olive Young’s online cosmetic sales to overseas markets soared 70% YoY in 1H 2025, fueled largely by the explosive demand from the United States.

We have raised our NAV valuation ofCJ Corp (KRX: 001040) to 207,713 won per share (up 28%). We raised the valuation of CJ Olive Young to 7 trillion won.

🇰🇷 APR: Time To Take Profits (Three Major Reasons) (Douglas Research Insights) $

There are three major reasons why we would take profits on APR Co Ltd (KRX: 278470) at current levels.

They include lofty valuations, increased competition, and share price decline post large scale dividend payout announcement.

APR could be facing especially tough competition for the beauty device products from Amorepacific Corp (KRX: 090430 / 090435) / Amorepacific Holdings (KRX: 002790), LG H&H (KRX: 051900 / 051905 / OTCMKTS: LGHMF), and others especially starting in 4Q 2025.

🇰🇷 M&A of Hyundai Hyms – Who Will Buy Controlling Stake? (Douglas Research Insights) $

The management ownership stake of Hyundai Hyms Co Ltd (KOSDAQ: 460930) is up for sale. J&P Private Equity firm which owns 52.88% stake in Hyundai Hyms has sent out teaser letters to potential buyers.

Including a management premium ranging from 30% to 50%, the potential acquisition price (including management premium) could be worth about 481 billion won to 555 billion won.

Since the second largest shareholder, HD Korea Shipbuilding & Offshore Engineering Co., Ltd. (KRX: 009540) (20.89% stake), has the right of first negotiation, the selling side must first negotiate with HD KSOE.

🇰🇷 Doosan Corp (000150 KS): Global Index Inclusion & A Relative Value Trade (Douglas Research Insights) $

A doubling of the stock price over the last 3 months could lead to Doosan Corp (KRX: 000150 / 000155 / 000157) being included in a global index in August.

Doosan Corp (000150 KS) has outperformed its peers over the last few months and now trades at a huge valuation premium to its peer group.

The stock is 17% off its recent highs and that provides an opportunity for a relative value trade heading into the index inclusion event.

🇰🇷 LG Energy Solution: Light At the End of the Tunnel? (Douglas Research Insights) $

LG Energy Solution (KRX: 373220) has been on a dark, long tunnel in the past two and half years. However, there is finally some light showing post its excellent 2Q 2025 results.

LG Energy Solution reported much better than expected operating profit in 2Q25. It had operating profit of 492.2 billion won (up 152% YoY) and 56.3% higher than consensus in 2Q25.

The company is showing initial signs of a turnaround, with a significantly better than expected operating profit in 2Q 2025.

🇰🇷 Samsung Electronics Clinches a Huge Chip Contract from Tesla (Douglas Research Insights) $

On 28 July, it was reported that Samsung Electronics (KRX: 005930 / 005935 / LON: BC94 / FRA: SSUN / OTCMKTS: SSNLF) clinched a huge chip contract worth $16.5 billion from Tesla (TSLA US).

This is a major win for Samsung Electronics since it is one of the largest foundry orders for the company from a single customer in the past decade.

Samsung Electronics is trading at attractive valuations. It is trading at P/E of 12.3x, P/B of 1.0x, and EV/EBITDA of 3.6x in 2026, based on consensus estimates.

🇰🇷 DH (Daehan) Shipbuilding IPO Book Building Results Analysis (Douglas Research Insights) $

DH Shipbuilding reported a solid IPO book building results analysis. The IPO price has been finalized at 50,000 won per share (high end of the IPO price range).

At the IPO price of 50,000 won, the expected market cap will be 1.9 trillion won. DH Shipbuilding will start trading on 1 August.

Our base case valuation of DH Shipbuilding is target price of 67,576 won per share, which represents a 35% upside to the IPO price.

🇰🇭 🇹🇭 Thailand and Cambodia agree to an immediate ceasefire in border fighting (Murray Hunter)

🇰🇭 🇹🇭 Satellite data indicates that Cambodia had a pre-determined plan before the conflict (Murray Hunter)

Back on the morning of July 24, the Cambodian response to a firefight between Thai and Cambodian soldiers at Ta Muen Thom Temple in Surin appeared to instantaneously escalate along the Thai-Cambodian border from Ubom Ratchathani to Sakaeo, over 150km spread. Such an escalation just doesn’t occur over such a long distance. There appears to be some pre-meditated plan behind the Cambodian actions.

A satellite data analyst Nathan Ruser from the Australian Strategic Policy Institute (ASPI) on his X account postulates from the data, that the Cambodian military had prepared for what happened months before. Nathan has run previous analysis on places like the Russian-Ukraine and China-India borders.

According to his analysis, most signs of military buildup and rising tensions appear to have originated on the Cambodian side. Cambodian military forces had reinforced various positions well before the May 28 incident and rapidly deployed strategic reinforcements immediately afterward.

🇰🇭 🇹🇭 Thai-Cambodian conflict expands to Trat province (Murray Hunter)

On July 25, a massive convoy of Thai armored personnel carriers and tanks were rushed to the Thai-Cambodia border. Thai forces are now poised to enter Cambodia, with F-16 air support to create a buffer zone and prevent anymore Thai civilian casualties along border towns. There are now approximately 100,000 evacuated Thais staying in camps, temples, and the homes of relatives deeper into Thailand.

Although both countries have withdrawn their respective ambassadors, there are still commercial flights between Bangkok and Phnom Penh continuing. This is perhaps one sign that both countries treat the fighting as border skirmishes up to now.

🇲🇾 Genting’s proposal for downstate New York resort is the largest of all bids in terms of casino-floor area: firm (GGRAsia)

Genting group’s [Genting Berhad(KLSE: GENTING / OTCMKTS: GEBHY)] proposal to develop a fully-fledged casino resort in downstate New York, in the United States, is the “largest of all the bids in terms of site size, build area, and casino-floor area,” according to a press release issued by the Malaysian-based group on Monday.

On Monday, Genting presented its plan (pictured in an artist’s rendering) to a six-person Community Advisory Committee, as part of the tender process for one of three licences potentially on offer.

Three groups with experience in running casinos in Asia – Genting group, MGM Resorts International (NYSE: MGM), and Mohegan Tribal Gaming Authority – are among eight bidders for one of three licences potentially on offer in downstate New York.

Genting group operates casinos in Malaysia, Singapore, Las Vegas, Nevada, and upstate New York. For its downstate New York bid, the firm is proposing to extend and upgrade its existing Resorts World New York City slot-machine and electronic gaming facility in Queens.

🇲🇾 Turun Anwar: a massive victory for PAS (Murray Hunter)

With an over whelming turnout to the “Turun Anwar” rally today centering on Dataran Merdeka, it was clearly evident who the winner was.

With the conspicuous absence of the “reformasi” crowd, the massive turnout was dominated by loyal followers of PAS, who came out from all parts of the peninsula.

PAS has come out in force making a symbolic statement that politics in Malaya will be different now. It wasn’t about prime minister Anwar Ibrahim leaving office. It was about who will rule Malaysia in the future.

🇲🇾 “Turun Anwar” rally was a tremendous success (Murray Hunter)

The “Turun Anwar” rally on July 26, 2025, was a tremendous success in terms of the numbers that turned out, the crowd stretching from Sogo to Masjid Negara, it was virtual ocean of crowd.

The conservative and deliberate attempts to convey picture of 10,000 to 15,000 participants pales in significance to the actual turnout from 150,000 to 200,000, even the slight shower did not dampen the enthusiasm of the crowd.

The Malays have made up their mind that Anwar has to go, the Chinese and Indians must decide sooner or later. Sitting on the fence expecting Anwar to emerge miraculously from the present crisis is nothing but a very tall and impossible order.

Anwar wants the opposition to take the parliamentary route to decide whether he should be the prime minister or not by passing a vote of non-confidence knowing very well that they don’t have the required numbers.

🇸🇬 Singapore Airlines hit by losses at Air India (FT) $🗃️

Singaporean carrier’s first quarter net profit plunges almost 60%

Singapore Airlines (SGX: C6L / FRA: SIA1 / OTCMKTS: SINGY / SINGF)suffered a 59 per cent drop in profits last quarter as it was hit by losses from its stake in Air India, the carrier embroiled in India’s worst aviation disaster in three decades.

Net profits at Singapore’s national carrier fell from S$266mn ($207mn) to S$186mn compared with the same period last year, the group reported on Monday. It said its losses from associated companies, “notably from Air India’s financial results”, were S$122mn for the three months to the end of June.

🇸🇬 The Straits Times Index Has Cracked the 4,200 Level: Is There Room for Further Gains? (The Smart Investor)

The index has repeatedly set new records this year as it chalks up double-digit gains. Could there still be legs for a further rally?

Earlier this month, the bellwether blue-chip index crossed the 4,000-mark for the first time as it recovered from April’s tariff announcement.

Just this week, the index has shot past the 4,200 level and shows no sign of stopping.

Can this rally sustain, or should investors stay cautious for now? We unpack these developments to bring you some insights.

A broad-based rally

Awaiting the banks’ results

Strategic reviews to unlock further value

Get Smart: Monitor the business closely

🇸🇬 5 Singapore Stocks Hitting Their 52-Week Highs: Can They Continue to Soar? (The Smart Investor)

🇸🇬 4 Singapore Blue-Chip Stocks Chalking Up Double-Digit Share Price Gains: Are They Worth Buying? (The Smart Investor)

🇸🇬 MAS is Injecting S$1.1 Billion into Small & Mid-Cap Companies: 5 Singapore Stocks That Could Benefit (The Smart Investor)

Back in February this year, the Monetary Authority of Singapore (MAS) announced the formation of an Equities Market Review Group (EMRG) that will work on measures to improve liquidity and valuations.

Just this week, MAS appointed the first three fund managers and will allocate an initial sum of S$1.1 billion under the Equity Market Development Programme (EQDP).

These funds have a mandate to improve liquidity on the local bourse and broaden participation in Singapore equities, with a focus on allocation to small and mid-sized companies.

Here are five such companies that we believe can benefit from this injection of liquidity.

Food Empire (SGX: F03)is a food and beverage (F&B) manufacturing and distribution group.

Isoteam Ltd (SGX: 5WF) provides repairs and redecoration (R&R) and additions and alterations (A&A) works with major customers including town councils, government bodies, and private sector building owners.

CSE Global Ltd (SGX: 544 / FRA: XCC / OTCMKTS: CSYJY / CSYJF)provides electrification, communications and automation solutions across different industries.

UMS Integration Ltd (SGX: 558 / OTCMKTS: UMSSF)provides equipment manufacturing and engineering services to original equipment manufacturers (OEMs) of semiconductors and related equipment.

Frencken Group Ltd (SGX: E28)provides comprehensive original design, original equipment, and diversified integrated manufacturing solutions.

🇸🇬 5 Singapore Stocks Yielding More Than Your CPF Ordinary Account (The Smart Investor)

However, did you know that the CPF Ordinary Account (OA) only pays you an interest rate of 2.5% per annum?

While this rate is nearly risk-free, it may not be sufficient to beat inflation over the long term, which averages around 2% to 3% per annum.

Here are five stocks that you can include in your CPF IA buy watchlist that have higher yields than the CPF OA account.

Nordic Group Ltd (SGX: MR7) is an engineering solutions provider serving the marine, offshore oil and gas, petrochemical, and infrastructure industries, to name a few.

China Sunsine Chemical Holdings (SGX: QES) is a speciality chemical producer selling rubber accelerants, insoluble sulphur, and other vulcanising agents.

Valuetronics Holdings (SGX: BN2 / FRA: GJ7)is an integrated electronics manufacturing services (EMS) provider supplying a full range of services from conceptualisation to engineering design and development.

HRNetGroup (SGX: CHZ)is a leading recruitment and staffing firm with over 900 consultants across 18 Asian cities.

Hotung Investment Holdings Ltd (SGX: BLS)is Taiwan’s leading venture capital investment management group.

🇸🇬 The Power of Long-Term Investing: 4 Singapore Stocks That Soared 290% or More in the Last 5 Years (The Smart Investor)

The benefits of long-term investing are on full display with these four solid growth stocks.

Here are four Singapore stocks that delivered impressive returns over the last five years.

The first stock on this list is Oiltek International Ltd (SGX: HQU), a company that provides a comprehensive and diversified range of refinery processes and engineering solutions across different sectors of the vegetable oils industry value chain.

Azeus Systems Holdings (SGX: BBW)sells software products and services and helps to deliver innovative IT solutions to companies and government agencies in more than 100 countries.

iFAST Corporation Limited (SGX: AIY / FRA: 1O3 / OTCMKTS: IFSTF) is a financial technology company operating a platform that allows for the buying and selling of unit trusts, equities, and bonds.

Centurion Corporation Ltd (SGX: OU8)is a provider of purpose-built worker accommodation (PBWA) and purpose-built student accommodation (PBSA) assets.

🇸🇬 4 Temasek-Owned Singapore Blue-Chip Stocks with Solid Long-Term Prospects (The Smart Investor)

The investment firm recently released its 2025 Annual Review and reported a 20-year total shareholder return of 7%.

This is an impressive performance considering the portfolio went through both the Global Financial Crisis and the recent COVID-19 pandemic.

We teased out four Singapore blue-chip stocks in which Temasek has a stake.

These companies all possess great prospects and should seriously be considered for your buy watchlist.

Sembcorp Industries (SGX: U96 / FRA: SBOA / OTCMKTS: SCRPF), or SCI, is an energy and urban solutions provider.

Keppel Ltd (SGX: BN4 / FRA: KEP / KEP1 /OTCMKTS: KPELY / KPELF)is a global asset manager with expertise in the infrastructure, real estate, and connectivity sectors.

Singapore Technologies Engineering Ltd (SGX: S63 / FRA: SJX / OTCMKTS: SGGKF), or STE, is an engineering and technology group that serves the aerospace, smart city, and defence sectors.

DBS Group (SGX: D05 / FRA: DEVL / DEV / OTCMKTS: DBSDY / DBSDF) is Singapore’s largest bank by market capitalisation and offers a wide range of banking, investment, and insurance services.

🇸🇬 Earnings Preview: 4 Singapore REITs That Will Likely Raise Their DPU (The Smart Investor)

REITs had a tough time in the last three years as interest rates soared and inflation reared its ugly head.

The result was lower distributions as REITs had to grapple with overall higher costs.

However, there is a select group of Singapore REITs that we believe can buck the trend.

Here are four that look well-positioned to continue raising their distributions.

Parkway Life Real Estate Investment Trust (SGX: C2PU), or PLife REIT, is a healthcare REIT with a portfolio of 75 properties located in Singapore (3), Japan (60), France (11), and Malaysia (1).

CapitaLand Ascendas REIT (SGX: A17U / OTCMKTS: ACDSF), or CLAR, is Singapore’s oldest industrial REIT with a portfolio of 226 properties worth S$16.9 billion as of 31 March 2025.

Keppel DC REIT (SGX: AJBU / OTCMKTS: KPDCF) is a data centre REIT with a portfolio of 24 data centres spread across 10 countries.

Mapletree Industrial Trust (SGX: ME8U / OTCMKTS: MAPIF), or MIT, is an industrial REIT with a portfolio of 141 properties spread across Singapore (83), the US (56), and Japan (2).

🇸🇬 Shopee’s Dominance in Southeast Asia’s E-Commerce Market (The Wolf of Harcourt Street)

The $128 Billion Market Opportunity

Southeast Asia platform e‑commerce gross merchandise volume (GMV) grew by 12% in 2024 to reach $128.4 billion. This growth was driven by continued internet adoption and rising consumer spending, led by Indonesia’s $56 billion market (44% of GMV). Thailand and Malaysia were the fastest-growing markets (~22% and 19% YoY, respectively).

Shopee entered 2025 as Southeast Asia’s #1 e‑commerce platform by volume, with a widening lead. It has achieved this through a combination of scale, infrastructure investment, and smarter monetization. With total GMV still rising and digital penetration far from mature, Shopee appears well-positioned for profitable growth.

Importantly, Sea Limited (NYSE: SE) is no longer burning cash to gain share. Instead, it is transforming Shopee into a high-volume, margin-expanding platform, a promising trajectory for long-term shareholders.

🇮🇳 MakeMyTrip: Still In The Driver’s Seat To Capitalize On The Demand Tailwind(Seeking Alpha) $🗃️

🇮🇳 HDFC Bank: Growth To Rebound From Here, Reiterate Hold Rating On Expensive Valuation(Seeking Alpha) $⛔🗃️

🇮🇳 Sify Technologies: An Execution Risk(Seeking Alpha) $⛔🗃️

🌐 Sify Technologies (NASDAQ: SIFY) – Largest ICT service provider, systems integrator & all-in-one network solutions company on the Indian subcontinent. 🇼

Recent Results: Q1 EBITDA surged 38% YoY to ₹7,576 Cr, driven by volume ramp-up, improved product mix, and lower coking coal costs.

FY26 Guidance: Company maintains production at 30.5 mt and sales at 29.2 mt, reflecting confidence in its ramp-up and downstream expansion roadmap.

Valuation & Growth: Trading at ~18× FY27E P/E and ~7× EV/EBITDA—above global peers—justified by projected 20% EBITDA and 23% EPS growth into FY27.

🇮🇳 Bajaj Finance CEO Resignation: Rajeev Jain Returns, But Succession Looms Large (Smartkarma) $

Anup Saha’s sudden resignation as MD of Bajaj Finance Limited (NSE: BAJFINANCE / BOM: 500034), just three months into the role, raises succession planning concerns.

The architect of BAF’s growth resumes full control as VC & MD until March 2028, ensuring near-term continuity.

While operations remain stable, the event sharpens focus on long-term leadership depth in India’s most premium NBFC.

🇮🇳 Sona Comstar’s China JV: Tapping into the World’s Largest EV Market (Smartkarma) $

On July 20, 2025, Lenovo Group (HKG: 0992 / FRA: LHL / LHL1 / OTCMKTS: LNVGY / LNVGF) announced a $20 million joint venture with China’s JNT to enter the world’s largest EV market.

The move aims to capture growth in China’s dominant EV market, aligning with the company’s new strategy to expand into eastern markets

An EV slowdown is expected in FY26 while the China JV and railway business, despite driving future growth from FY27 onwards, are expected to lower margins.

🇮🇳 DLF’s Mumbai Re-Entry: A New Era for Premium Real Estate? (Smartkarma) $

DLF Ltd (NSE: DLF / BOM: 532868) re-entered Mumbai after a decade with ‘The Westpark’, a luxury project in Andheri West, featuring 416 apartments and INR 800-900 crore investment

Company launched a Mumbai luxury project targeting INR 2,000-2,300 crore revenue from phase one, with broader market expansion and new launch plans

This signals a strategic shift for debt-free DLF towards high-margin luxury developments, leveraging Mumbai’s booming market and demand for premium homes

Natco Pharma Ltd (NSE: NATCOPHARM / BOM: 524816) acquires a 35.75% stake in South Africa’s Adcock Ingram Holdings Limited (JSE: AIP), marking its largest overseas expansion to date.

This move instantly gives Natco a strong foothold in Africa’s pharma market and diversifies its global revenue streams from current headwind of US market.

Natco transitions from a primarily India/US-focused player to a serious contender in strategic emerging markets, enhancing its growth outlook.

🇮🇳 Event Driven: Tilaknagar Ind ₹4,150 Cr Imperial Blue Acq.~Transformational Play or Leverage Trap? (Smartkarma) $

Tilaknagar Industries Ltd (NSE: TI / BOM: 507205) acquires Pernod Ricard India’s Imperial Blue for INR 4,150 crore, diversifying its portfolio into whisky from dominance in brandy.

This acquisition will establish TI as a pan-India spirits player, significantly enhancing distribution and is expected to be accretive.

However, substantial deal size raises concerns about equity dilution, high leverage risks, and significant integration challenges for TI

🇮🇳 NSDL IPO Analysis: India’s First & Largest Depository (Smartkarma) $

National Securities Depository Limited (NSDL)’s IPO is an OFS priced at INR 760-800 per share, targeting an issue size of INR 3,810-4,011 crore

As India’s pioneering SEBI-registered MII, company is the largest depository, serving 79,773 issuers as of March 2025, driven by market growth and innovation.

Valuation indicators suggest a fair assessment relative to industry peers, underscored by a robust issuer base and inherent financial stability.

🇰🇿 The Most Asymmetrical Large Cap Stock I’ve Ever Found (Peter’s Substack)

An incredibly high-quality value investment in an environment full of greed

I’ve done more research on KASPI (NASDAQ: KSPI / LON: 80TE / FRA: KKS) than any other investment, and I believe it’s the most asymmetrical opportunity among large caps and bigger. It’s a one-of-a-kind situation that most won’t take seriously — and I believe that’s a mistake.

Kaspi is the first and only company from Kazakhstan to list its shares on U.S. exchanges. It’s essentially a conglomerate, but you can broadly sum up its businesses into banking, payment processing, and e-commerce.

Saudi Arabia had long known that it had a weakness: Food. Seeking to end its dependency on food imports, Saudi Arabia in 1980 embarked on a massive self-sufficiency program fueled by oil money and fossil water. That program eventually focused on a single water thirsty crop: Wheat. Things got a bit out of control. In the mid-1980s and early 1990s, Saudi Arabia pumped more groundwater than oil. And 5% of the entire 1991 Saudi budget was being spent on growing more wheat than anyone can eat. In today’s video, a noble policy with long-running water consequences.

🇿🇦 Gold Fields: Valuation No Longer Attractive(Seeking Alpha) $⛔🗃️

🌐 Gold Fields (JSE: GFI / NYSE: GFI) – One of the world’s largest gold mining firms. 9 operating mines in Australia, Peru, South Africa & Ghana (including the Asanko JV) & 2 projects in Canada & Chile. 🇼🏷️

🌎 Ternium S.A. (NYSE: TX) 🇱🇺 – Manufactures & processes steel products (including for oil & gas) with 18 production centers in Argentina, Brazil, Colombia, United States, Guatemala & Mexico. Subs. of Argentine-Italian conglomerate Techint. 🇼🏷️

🌎 Globant: AI Risk Appropriately Priced In (Seeking Alpha) $⛔🗃️

🌎 Mercado Libre: Leading LatAm’s Digital Economy Through E-Commerce and Fintech Synergy (Compounding Your Wealth)

Deep Dive into MercadoLibre (NASDAQ: MELI): Valuation, Segment Growth, Key Metrics, Profitability, Expenses, Product Launches, Customer Acquisition, Financial Stability, SBC/Revenue, and Shareholder Dilution.

Valuation appears attractive, with low Forward EV/Sales and reasonable Forward P/E multiples, supported by a durable competitive advantage. Management’s strategic bet on Argentina is paying off—following the stabilization of the economy, revenue in the region is now growing at triple-digit rates.

The share of Non-Performing Loans (NPLs) over 90 days has improved significantly since Q4 2022, as the company continues to stabilize credit quality—a trend that has also contributed to a decline in NIMAL.

🌎dLocal: The Hyper-Local Fintech Powering Emerging Markets (Penny Insight)

A deep dive into Dlocal (NASDAQ: DLO)’s business model, competitive edge, and why its 83% stock drawdown may be a long-term buying opportunity.

Despite being a consistently profitable and cash-generative business, dLocal’s stock has fallen more than 83% from its all-time high—underscoring the disconnect between strong fundamentals and market perception. To assess whether this sell-off is justified or a long-term opportunity, it’s essential to understand how dLocal operates at its core.

With disciplined capital allocation, expanding geographic licenses, and a credible new CEO in Pedro Arnt, dLocal is entering a new phase. If the company can maintain its growth trajectory and improve margin discipline, it doesn’t need to return to past highs to generate strong shareholder returns. At today’s valuation, even partial re-rating or earnings expansion could drive meaningful upside—offering a potentially asymmetric setup for investors willing to stomach near-term volatility in pursuit of long-term compounding.

🌎DLocal: A Great Bet On Emerging Markets And FinTech (Seeking Alpha) $⛔🗃️

🇦🇷 Luxury Boom in Milei’s Argentina Masks Despair Among the Masses (Bloomberg) $ 🗃️

🇦🇷 Argentine Banks: Volatility Is Not A Symptom Of Weakness, But Part Of The Ecosystem(Seeking Alpha) $⛔🗃️

🇧🇷 Chinese Car Giants Rush Into Brazil With Dreams of Dominating a Continent (NY Times) $ 🗃️

🇧🇷 TIM S.A. Q2 Earnings Preview: Unspoken Risks(Seeking Alpha) $⛔🗃️

🇧🇷 Embraer And The U.S. 50% Tariff On Brazil: How Bad Could It Get? (Rating Downgrade)(Seeking Alpha) $⛔🗃️

🇧🇷 Pump Up Your Portfolio With Petrobras(Seeking Alpha) $⛔🗃️

🇧🇷 Banco do Brasil: Tariff Headwinds Will Continue To Put Pressure On Agribusiness Lending(Seeking Alpha) $⛔🗃️

🇧🇷 StoneCo Stock Has A Clear Path To $30 (Seeking Alpha) $🗃️

🇨🇱 World’s largest copper producer says Trump’s tariffs are causing ‘anxiety’ (FT) $ 🗃️

🇨🇱 Sociedad Química y Minera de Chile: A De-Risked Giant For The Coming Lithium Bull Market(Seeking Alpha) $🗃️

🌐 Nebius Group: A Rare Early Stage Shot At A GPU Superpower In The Making (Seeking Alpha) $⛔🗃️

🌐 Nebius: Everyone Talks About AWS And Azure – But This Tiny Player Is Gaining Ground (Seeking Alpha) $🗃️

🌐 Nebius Group NV (NASDAQ: NBIS) – AI-centric cloud platform built for intensive AI workloads. Sold Yandex to a consortium of Russian investors. Retains several businesses outside of Russia. 🇼🏷️

Share

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

Click here for the full weekly calendar from Investing.com containing frontier and emerging market economic events or releases (my filter excludes USA, Canada, EU, Australia & NZ).

Frontier and emerging market highlights (from IFES’s Election Guide calendar):

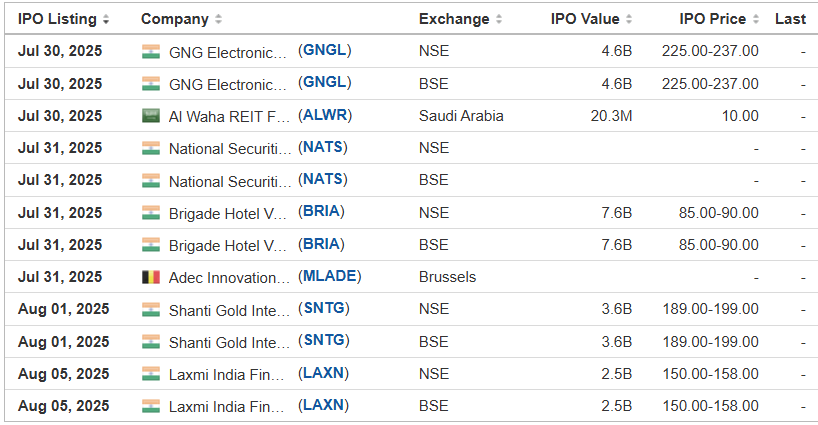

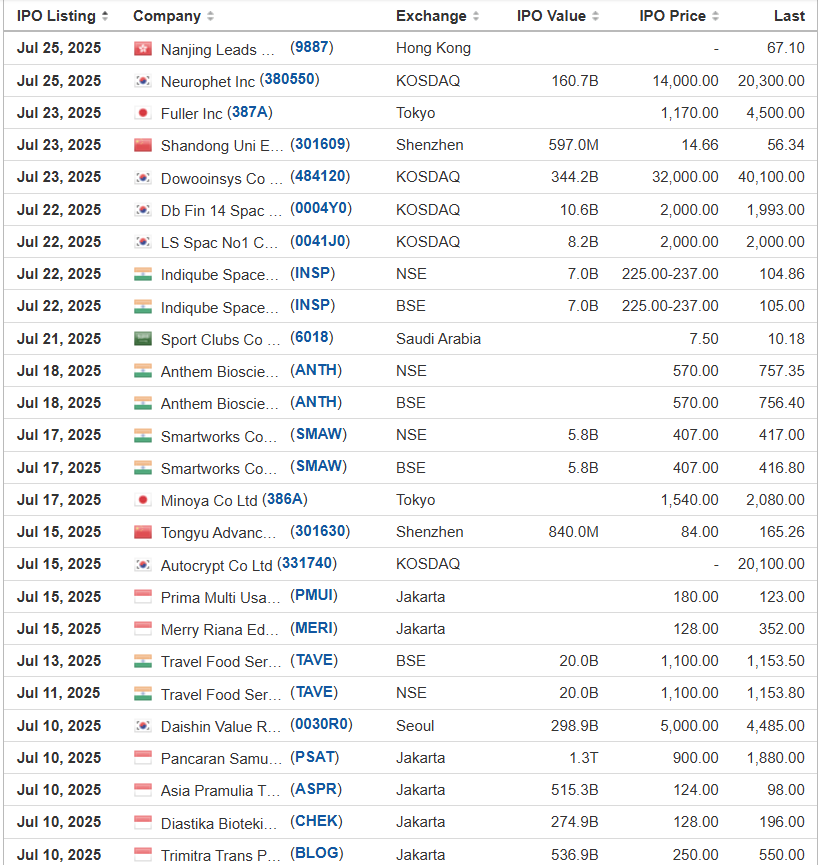

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

BUUU Group LimitedBUUU Dominari Securities/Pacific Century Securities/Revere Securities, 1.5M Shares, $4.00-6.00, $7.5 mil, 8/1/2025 Week of

(Incorporated in the British Virgin Islands)Established in 2017, we have rapidly grown into a premier Meetings, Incentives, Conferences, and Exhibitions (“MICE”) solutions provider based in Hong Kong. Our comprehensive marketing service portfolio is designed to meet the diverse needs of our clients, spanning across two core areas: (i) event management and (ii) stage production.(a) Event management servicesIn the realm of event management, our operating subsidiary, BU Creation, excels as creative planners and meticulous executors. We curate and manage a wide spectrum of events, including cultural, artistic, recreational, and corporate promotions. Our approach is deeply collaborative, and we work closely with our clients to bring their visions to life. From the initial concept to the final execution, we ensure every detail is aligned with our clients’ objectives, delivering events that resonate and captivate audiences. In addition, we have collaborated with event production houses to co-host various remarkable events in Hong Kong. Notable examples include the S2O Songkran Music Festival Hong Kong, the Spartan Race Hong Kong, and the Grade 10 Asia Card Show Hong Kong.Under our event management services, BU Creation directly engages in (i) design and planning, (ii) project management, and (iii) on-site supervision.Our revenue derived from event management services represents approximately 77.9% and 77.5%, and 80.5% and 72.2% of our total revenue for the six months ended December 31, 2024. and December 31, 2023, and the years ended June 30, 2024, and June 30, 2023, respectively.(b) Stage production servicesOur expertise in stage production lies in our ability to transform spaces into immersive experiences. Our operating subsidiary, BU Workshop, meticulously coordinates with suppliers to integrate advanced lighting, visual and audio systems, stage performance elements and venue decorations. Our goal is to create environments that not only engage but also leave a lasting impression, elevating the impact of every event we manage.Under our stage production services, BU Workshop directly manages the entire production process, from stage management and technical direction to the fabrication and installation of set elements. The lighting and visual and audio systems involved are sourced from its suppliers.Our revenue derived from stage production services represents approximately 22.1% and 22.5%, and 19.5% and 27.8% of our total revenue for the six months ended December 31, 2024, and December 31, 2023, and the years ended June 30, 2024, and June 30, 023, respectively.Our diverse clientele includes public institutions, marketing and public relations firms, real estate corporations, and a number of established brands. This broad customer base reflects our ability to deliver customized solutions that meet the high standards of various sectors.Note: Net income and revenue are for the 12 months that ended June 30, 2024.(Note: BUUU Group Limited is offering 1.5 million shares at a price range of $4.00 to $6.00 to raise $7.5 million, if priced at the $5.00 mid-point of its range, according to its SEC filings.)

Climate change and ESG are some recent flavours of the month for most new ETFs. Nevertheless, here are some new frontier and emerging market focused ETFs:

04/02/2025 – Goldman Sachs India Equity ETF – GIND

03/21/2025 – FT Vest Emerging Markets Buffer ETF – March – TMAR

03/15/2024 – Polen Capital China Growth ETF – PCCE – Active, equity, China

03/04/2024 – Simplify Tara India Opportunities ETF – IOPP – Active, equity, India

02/07/2024 – Direxion Daily MSCI Emerging Markets ex China Bull 2X Shares – XXCH – Equity, leveraged, China

01/11/2024 – Matthews Emerging Markets Discovery Active ETF – MEMS – Active, equity, small caps

01/10/2024 – Matthews China Discovery Active ETF – MCHS – Active, equity, small caps

Frontier and emerging market highlights:

Check out our emerging market ETF lists, ADR lists (updated) and closed-end fund (updated) lists (also see our site map + list update status as most ETF lists are updated).

I have changed the front page of www.emergingmarketskeptic.com to mainly consist of links to other emerging market newspapers, investment firms, newsletters, blogs, podcasts and other helpful emerging market investing resources. The top menu includes links to other resources as well as a link to a general EM investing tips / advice feed e.g. links to specific and useful articles for EM investors.

Disclaimer. The information and views contained on this website and newsletter is provided for informational purposes only and does not constitute investment advice and/or a recommendation. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content. Seek a duly licensed professional for any investment advice. I may have positions in the investments covered. This is not a recommendation to buy or sell any investment mentioned.

Emerging Market Links + The Week Ahead (July 28, 2025) was also published on our website under the Newsletter category.

")