Net interest margin (NIM) improved a shade to 4.30 per cent in Q2FY26 from 4.27 per cent in the preceding quarter, but was lower than 4.34 per cent in the preceding quarter

| Photo Credit:

REUTERS

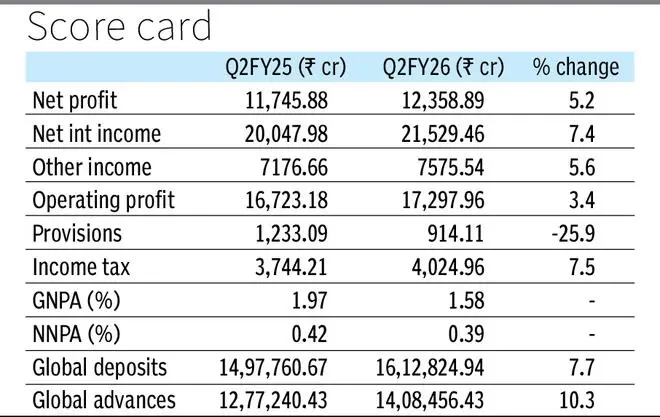

ICICI Bank reported a modest 5 per cent year-on-year (y-o-y) growth in the second quarter (Q2FY26) with standalone net profit at ₹12,359 crore amid a decline in provisions, including towards non-performing assets (NPAs) and further improvement in asset quality.

India’s second largest private sector bank had recorded a net profit of ₹11,746 crore in the year ago quarter.

Net interest income (difference between interest earned and interest expended) in the reporting quarter was up 7 per cent y-o-y at ₹21,529 crore (₹20,048 crore in the year ago period).

Other income, including fee-based income, treasury income and recovery in written-off accounts, rose about 6 per cent y-o-y to ₹7,576 crore (₹7,177 crore).

Net interest margin (NIM) improved a shade to 4.30 per cent in Q2FY26 from 4.27 per cent in the year ago quarter, but was lower than 4.34 per cent in the preceding (Q1FY26) quarter.

Sandeep Batra, Executive Director, observed that NIM is likely to remain rate-bound, with some benefits expected because of further (staggered) CRR (cash reserve ratio) cuts and repricing of deposits.

“From our perspective, we look at the overall profits from our relationship. So, it’s not only about the NIMs. We look at the fees…And of course, if there is a rate cut, there will be some nominal impact…on the NIMs as well,” he said.

Gross non-performing assets (GNPAs) position improved to 1.58 per cent of gross advances as at September-end 2025 against 1.97 per cent as at September-end 2024. Net NPAs position too improved a shade to 0.39 per cent of net advances against 0.42 per cent.

Domestic loans grew 10.6 per cent y-o-y. Within this, retail and corporate loans witnessed a relatively slow growth of 6.6 per cent and 3.5 per cent, respectively. Business banking grew a robust 24.8 per cent. Total advances, including domestic and overseas advances, were up 10.3 per cent to stand at ₹14,08,456 crore as at September-end 2025.

“Given all the policy measures, both from fiscal and monetary policy perspective, …we do expect the second half to be better….and we really remain positive on the overall loan growth going forward,” Batra said.

Total deposits rose 7.7 per cent y-o-y to stand ₹16,12,825 crore as at September-end 2025. The proportion of average current account, savings account (CASA) in domestic deposits improved to 39.2 per cent as at September-end 2025 from 38.9 per cent as at September-end 2024.

Published on October 18, 2025